What You Need To Qualify For DSCR Loan

- Investor-focused

- No personal verification

- Built for rental cash flow

DSCR Loan Requirements

at a glance

Borrower profile

Your investment experience, credit profile, and overall financial stability as a real estate investor.

Property cash flow

The property’s rental income vs. expenses is the core factor in DSCR loan approval.

DSCR ratio

Measures property income vs. debt. Most lenders require a DSCR of 1.0+.

Rental property details

Property type, location, condition, and market rental demand all impact loan eligibility.

Required documents

Lease agreements, rent estimates, property details, and basic financial documents to support the loan application.

Borrower requirements

Real estate investment experience

Experience managing rental properties or real estate investments can strengthen your application, especially when scaling your portfolio.

Business entity information

DSCR loans are often issued to LLCs or business entities, so you may need to provide entity formation documents and ownership details.

Credit profile

Your credit score and financial history help lenders assess reliability, even when personal income is not the primary factor.

Liquidity & cash reserves

Lenders may require proof of reserves to ensure you can cover vacancies, expenses, or unexpected costs.

Property requirements

DSCR loans are based on how well a property generates rental income.

Lenders evaluate its performance, stability, and market demand.

Eligible property type

Single-family rentals, condos, townhomes, and small multi-unit properties commonly qualify for DSCR financing.

Rental income potential

The expected monthly rent plays a key role in determining loan eligibility and overall cash flow.

Lease & occupancy status

Existing leases, tenant stability, and occupancy rates help lenders assess income consistency.

Market rent & demand

Local rental demand and comparable rent data are used to validate income projections and long-term performance.

Rental Income & Cash

Flow Requirements

DSCR loans are based on how well your property generates income. Lenders

review rental performance, projected income, and cash flow stability.

Monthly rental income

Provide current lease agreements or estimated rental income based on market rent to demonstrate earning potential.

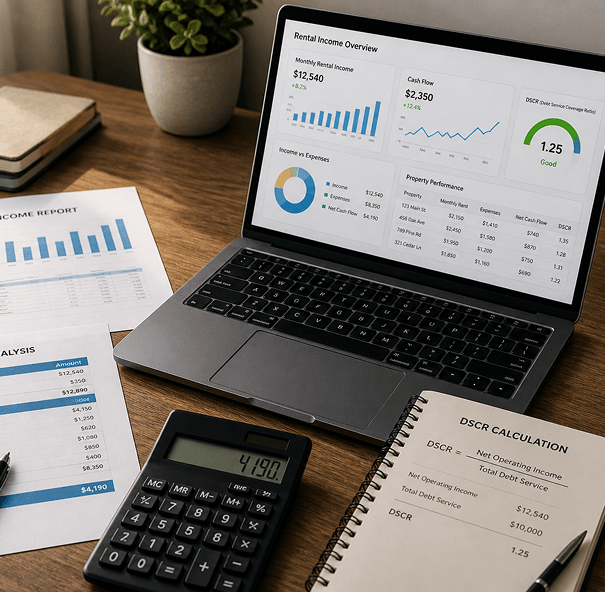

DSCR calculation

Lenders calculate the Debt Service Coverage Ratio (DSCR) to measure how rental income compares to loan payments.

Rental estimates & market data

Appraisals or rent schedules help validate expected income using comparable properties in the same area.

Cash flow stability

Consistent rental income and stable occupancy improve approval chances and loan terms.

DSCR Loan Metrics

At A Glance

Key financial factors lenders review to evaluate rental income,

loan coverage, and overall property performance.

Monthly rental income

The property’s expected or monthly rent used to determine loan eligibility.

DSCR ratio

How rental income compares to loan payments. DSCR 1.0+ is typically required.

Loan-to-value (LTV)

The percentage of property value financed, often up to 75–85%.

Loan-to-cost

How much of the purchase and renovation cost may be financed.

Cash reserves

Funds set aside to cover vacancies, expenses, or unexpected costs.

Interest rate & terms

Loan pricing and repayment terms based on property performance and risk profile.

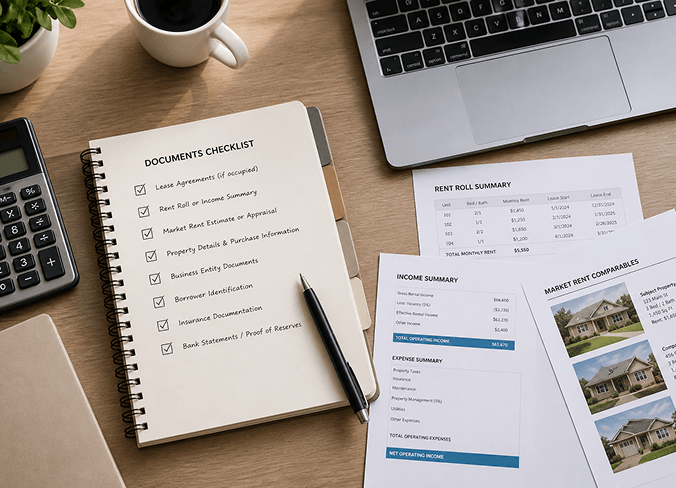

Documents to prepare

before applying

- Lease agreements (if occupied)

- Rent roll or income summary

- Market rent estimate or appraisal

- Property details and purchase information

- Business entity documents

- Borrower identification

- Insurance documentation

- Bank statements or proof of reserves

- Proof of insurance or builder's risk insurance

What can affect your loan approval?

Does investor experience matter for DSCR loan approval?

How does property condition affect DSCR loan eligibility?

What DSCR ratio is typically required?

Why is rental income stability important for a DSCR loan?

Do I need cash reserves to qualify for a DSCR loan?

How Brickline helps investors prepare

Rental income review

We help you evaluate your property’s rental income and estimate your DSCR before applying.

Requirement guidance

Know exactly what documents and income details are needed to avoid delays in your application.

Investor-focused process

Our process is built for rental property investors simple, fast, and aligned with real investment goals.

Clear next steps

Get a clear path from application to approval, including what to expect at every stage.

DSCR Loan

Requirement FAQs

What do I need to apply for a DSCR loan?

Do I need personal income or employment verification?

What is a good DSCR ratio?

How fast can I get approved?

Can I use a DSCR loan for multiple properties?

Ready to finance Your Next Rental Property?